Well, that was a week for the ages- both in terms of market moves and of course events. rarely does the Fed meeting play second fiddle to events but last week it clearly did with the election front and center.

Now we just have to figure out what lies ahead, and this week's diary focuses on just that.

What are the drivers now and how do markets look?

Let's start with the election. We know for sure that Donald Trump is the President elect as the 47th President of the United States. We also know for sure that the Republicans will control the senate.

If you believe "Decision Desk" (as you probably should given how they pretty much got everything in this election right so far) 216 seats are a lock at this point in the house for the Republicans. In addition, they assess an 82% probability that the Republicans will control the house with a likely 220 projected seats. I am guessing that probably gets solidified next week.

So, the first observation I will make is that Jay said any policy decisions would likely be impacted only by legislation put in place rather than projected. I would respectfully disagree with him on that. A Red Sweep makes it a virtual certainty that we will very quickly see that stated Fiscal and regulatory policies put in place.

Do you really want to keep cutting rates on the basis of what you are seeing today when you know full well what is coming around the corner?

These policies will undoubtedly be a shot in the arm to economic activity that was largely not entertained as recently as last week.

I argued before last week's Fed meeting that optionality would be put back on the table. What I meant by that is there was no way they could credibly change the decision to ease last week given the recent employment and inflation data and their guidance. To do so would have been viewed as "highly political"

I have also argued that both at last week's meeting and even more at the prior one that the Fed would do whatever Jay wants to do and that was certainly vindicated by the 50 bp's move in September. Ahead of that meeting it was clear that the Employment picture was concerning to him and in particular the sharp revisions lower in NFP for the April 2023- March 2024 period.

I hear a lot of people saying that Jay was dovish last week and again I respectfully disagree.

Back in 2021 we had a Fed that was very focused on one side of their dual mandate- Employment. As a consequence, they continually argued that inflation was transitory despite the fuel of supply shocks, huge fiscal stimulus and continued monetary stimulus.

Then as they saw the whites of the eyes of inflation that remained sticky, generated second round effects and went to levels not seen for decades they shifted to the other side of the mandate- inflation.

As we came into this year the subtle shift began again as the focus drifted to a more balanced focus with employment again being on the ascendancy. Prior to the September meeting it was now all about employment and we got Waller's 4-month annualized Core PCE of 1.8% to emphasize this in a description that was very selective.

With the September print we saw the 4-month annualised rate back up to 2.4%, the 3- month at 2.3%, the 6-month also close to 2.3% and the 12- month at 2.7%.

In the next 3-months the numbers that will come out of the calculation (Oct-dec 2023) as respectively .13%, .09% and .18% for an average of 0.13% a month while the last 3 months have averaged 0.19%. So, we have a very real possibility that annualised Core PCE is going to rise over this period - maybe even to a headline grabbing 3% again.

In addition, next week we get CPI numbers on Wednesday. with an expected .3% print MOM and 3.3% YOY. The trend of the last four months here is .1/.2/.3/.3 which annualizes at 2.7% and if we print 0.3% as expected next week that will take the 3-month annualized rate to 3.6% with the 6-month annualized at around 2.8%.

Jay told us that the inflation language was taken out because it referred to the position going into the last fed meeting i.e. "The Committee has greater confidence that inflation is moving sustainable towards 2%." In other words that language was only in there to support the decision to go 50 bp's. Once again, the Fed is providing a narrative to support what they (Jay) wanted to do.

Now the statement says that "The Committe judges that the risks of achieving its employment and inflation goals are roughly in balance"

So, the "Dual mandate" is back. policy is no longer driven primarily by inflation (2022-2023) or Employment 2020-2021 and 2024 but by both.

So now the inflation prints, the employment prints and by definition the fiscal/regulatory changes coming and their feedback loops are all in play in terms of policy decisions.

What does that mean for DECember

Given what I have said above, absent another shocker in the Employment report (which of course is possible) I find it hard to envisage the 50 bp's cut that my old colleagues at Citi are expecting especially as the inflation base effects make it a higher bar to see annualized rates falling in the next 3 months.

I would personally ascribe a much greater danger of a ZERO move at this point in December than a 50 bp's move.

I think what both the Fed statement and Jay's press conference provided was "cover" ie Optionality not to move in December.

A move at this point has to be considered as the base case BUT let us not forget that the base case in September changed because circumstances changed, and the Fed showed that it is finally prepared to adjust as they, rather than the market, sees fit.

IF inflation comes in well behaved/soft into the next meeting and the employment report is mediocre/soft then the 25 bp's move likely gets solidified.

But, what if we get

-A Red Wave (high probability)

- An inflation picture that prints higher than expected (not outside the realm of possibility) We will have 2 CPI reports before the meeting as well as 1 Core PCE report.

-A better employment report than expected (anything is possible in any given month). I remain very skeptical about the huge growth in Government jobs two months ago than substantially lowered the unemployment rate but that will not get revised out anytime soon.

- The almost certain knowledge that the incoming fiscal stimulus, potential tariffs, regulatory easing is going to be stimulatory for the economy and likely raise the specter of firming demand inflation upwards again.

In that instance would the Fed really cut rates?

The only real reason at that point to do so would be the fear that it could still looks political. But if that were the case I think it would have to be balanced by very clear guidance that a pause in January was more of a base case.

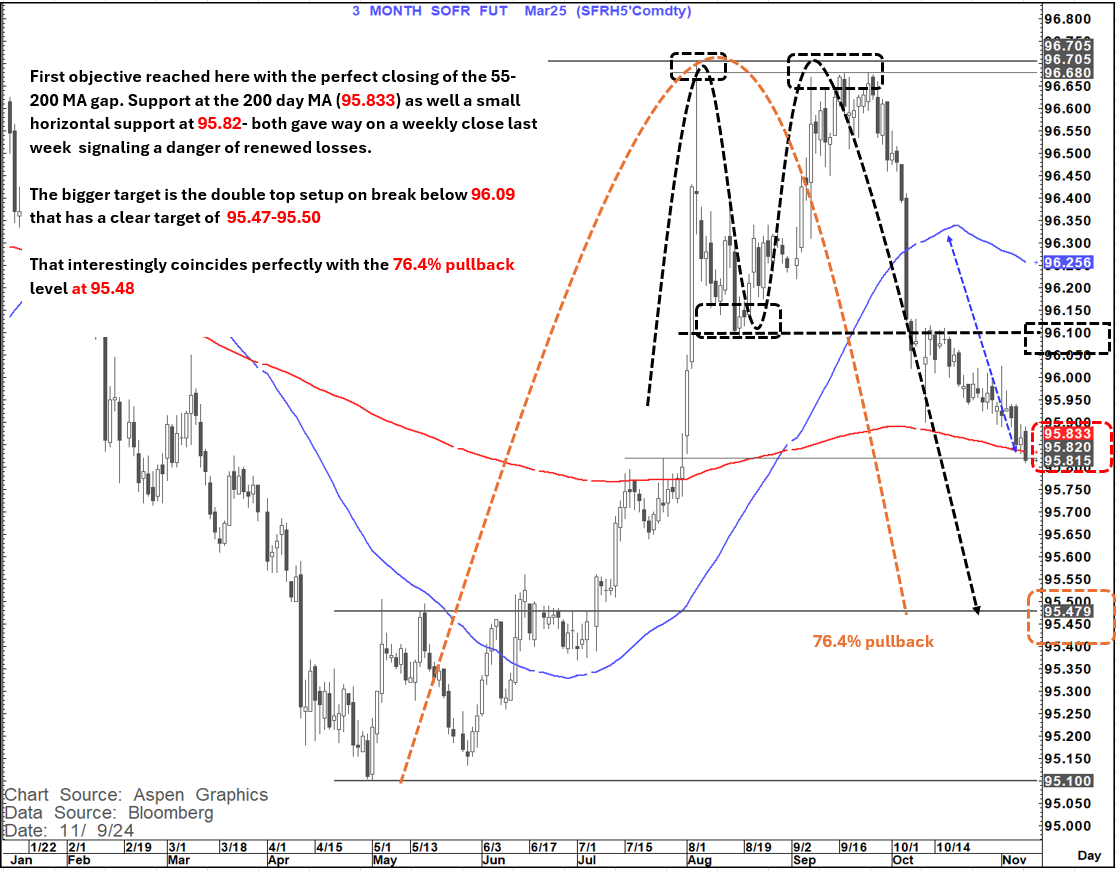

At this point the building blocks are clearly such that it would be hard to trade for the DEC pause but the chart below is really compelling for suggesting a real danger that we get guided towards a post DEC pause.

This is the March 2025 SOFR contract and the suggestion here is that there is a real danger that we move towards 95.48 which is about 38 bp's below Friday's close. This would clearly suggest a market adjusting its expectations for the future Fed path.

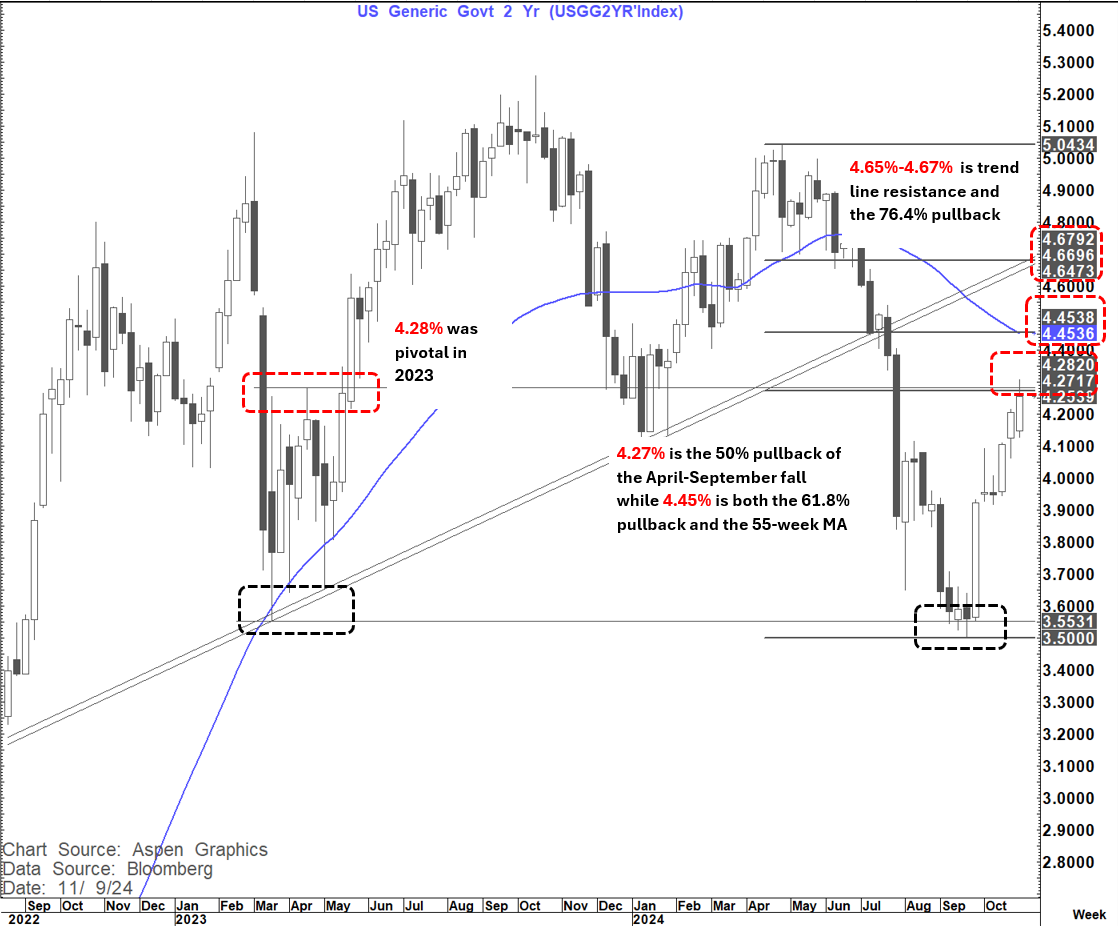

I have, in addition, for some weeks been arguing the danger that the US 2-year yield could head higher with an initial target of 4.27-4.28% (hit and slightly exceeded last week but not with a weekly close above)

Above there suggests a move to 4.45% + with an outside chance of even higher towards 4.65-4.67%+

While the move above 4.40% can easily be seen on the back of a suggested pause I think the move above 4.60% is a higher bar. That would likely need a market starting to believe this is looking more like a 1998 'esque 75 basis points and done easing cycle.

It is far too early at this point surmise such an outcome.

This overview above is also clearly problematic for the recent steepening curve moves that we have seen.

This is evidenced by the fact that we saw new lows in the 2's 5's and 2's 30's down moves last week as well as a bearish outside week in the 2's 10's curve.

Until we reach a new equilibrium in the 2-year yield the danger is that these curves could flatten further.

Bottom line we are moving into a very fluid time in times of markets, politics, Geopolitics and the economy and NOTHING can be taken for granted here.