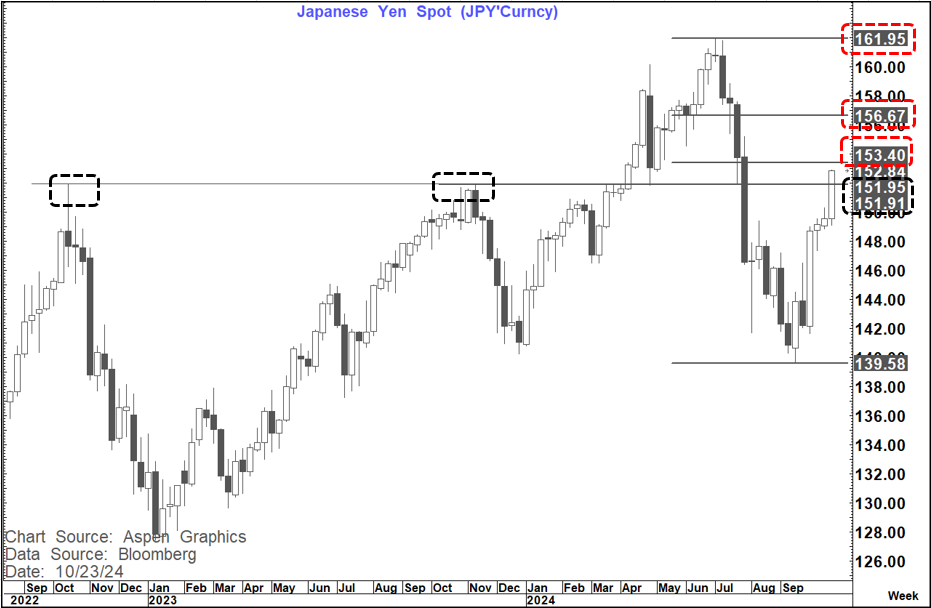

The are a number of interesting developments overnight BUT the first shout out has to go to USDJPY. Not only did it break above the 200-day MA at 151.38 but it is back above the prior double highs from Oct 2022 and October 2023 at 151.95 and 151.92. As an aside that is also interesting as those peaks occurred at the same time as US long end yields peaked - something I do not think is happening this time as per my piece yesterday Déjà vu Or Different This Time

Levels to watch now on USDJPY are 153.40 (61.8% pullback), 156.67 (76.4% pullback) and 161.95 (trend high)

The reality is that the present move in USDJPY is exactly in tandem with the US-Japan 5-year yield spread with this last pop just a "catch up". If you believe, as I do, that US yields are heading higher still then it is hard to go against this USDJPY move.

JPY crosses are also rallying but this is not really a "cross move" as the USD is bid across the board.

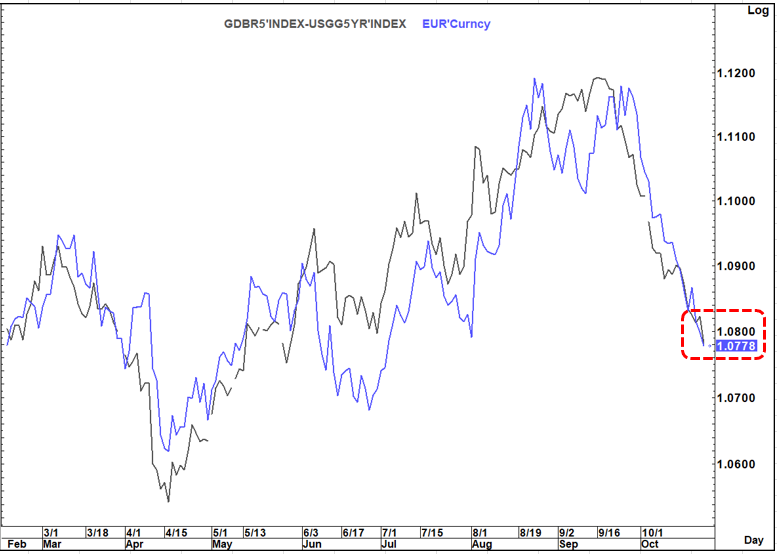

As can be seen below the path of EURUSD has also been closely following the relative 5-year yield spread and again IF this is heading lower still then likely so is EURUSD

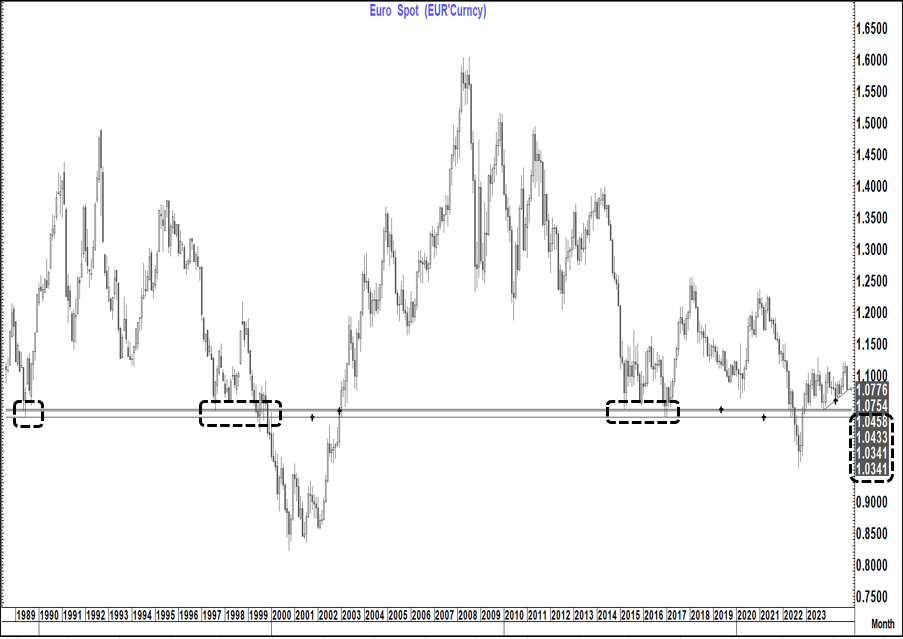

We do have some good support at 1.0746-50 (76.4% pullback and rising trend line) and then horizontal support at 1.0666 and 1.0601 . However if, as I expect, this spread continues to widen (even more compelling story as the gap between the ECB and the Fed is also widening) then we have to entertain the idea of EURUSD heading back to test long-term support around 1.0340-1.0460.

This USD bid tone is becoming widespread (USD-Index, BBDXY, AUDUSD, NZDUSD, USD-Asia (ex Japan), USDMXN (target 20.55), USDBRL (Potential target 6.00) etc

Yields are the driving force and I have focused in particular on the US 30-year yield which has led the way in this move and covered this with yesterday's piece Parting Is Such Sweet Sorrow

It continues to test the downward sloping resistance at 4.51% and a weekly close above would suggest a test of the double bottom neckline at 4.85%

In addition, overnight, the US 2's 5's curve has posted a marginal new high in the trend above resistance at minus 3 to minus 5 basis points ( 200-week MA). the next good resistance is met at +8 to +9 bp's but the ultimate double bottom target still remains +36 to +37 bp's

Other parts of the curve (2's 10's, 2's 30's in particular) also look set to move higher

This could get tempered with a pause/consolidation If the 2-year yield breaks HUGELY pivotal resistance at 4.09-4.13%.

A weekly close above this range, IF SEEN, would be very material as it would suggest an extension towards 4.4%+

The only likely cause of such a move (in my view) would be that the market begins to further price out Fed rate cuts as we head into November-December.

There has been a lot of pushback to the 50 bp's "Jay move" in September and with the election on Tuesday the 5th November it's result could be important in the Fed's process. If preceded by another "strong" pre-election employment report, we might have to call Vice Chair Timiraos back into action

Gold right now seems immune to the USD and yield moves and continues to make new highs. The $3,000 target remains firmly intact here.

WTI traded above, but could not sustain on a closing basis the $72.50 level. If we regain that level on a closing basis it would suggest a move back towards the high $70's . Such a development, if seen, would also likely further fuel the move higher in yields,

On Es1 the triple negative momentum divergence remains intact on the daily chart suggesting at least 5,830 again. IF we saw a close below that level then extended losses towards 5,721 to 5,725 would have to be entertained.

Bitcoin still seems to trade more like a risk asset than a risk hedge and is moving pretty much in tandem with the equity market

Copper (Hg1) has managed to sustain above supports at 430.50-432.45 on a weekly close basis and could still be forming a base here. A weekly close below this range, if seen, would question that potential.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}