The ECB has moved to being one of the most dovish central banks out there and it makes sense.

Headline inflation has dropped to 1.7% YOY.. BUT will surge again in the coming months due primarily to base effects. We have generally low numbers falling out in the next 4 months but in particular we have a minus 0.6 coming out in November and a minus 0.4 coming out in January. So, this number could bounce up to the high 2's and maybe close to 3%. Then it will fall again on the high base effects of Feb-April last year (+0.6/+0.8 and +0.6) OR WILL IT? More on that later.

While Core CPI is above the target at 2.7% it is at the low of the cycle having fallen from 5.7% in March last year. BUT Core CPI is a lagging/secondary effect

PPI (Excluding construction ) is at minus 2.3% YOY BUT has actually been rising since Sept last year when it printed YOY at minus 10.10%. The last 3 monthly prices have been +0.6, +0.7 and + 0.6 respectively (About +8% annualised)

There is no growth in the Eurozone (that is not, despite the pontifications of many ECB members, a "soft landing" . It is a "soft economy". The average annualized quarterly growth since Q2, 2023 has been just over 0.3% and with China in the doldrums a major outlet for growth looks compromised.

Unemployment stands at 6.4%- a low in the cycle for sure but elevated by any standards.

Where would the Fed have rates if we had these numbers?

BUT

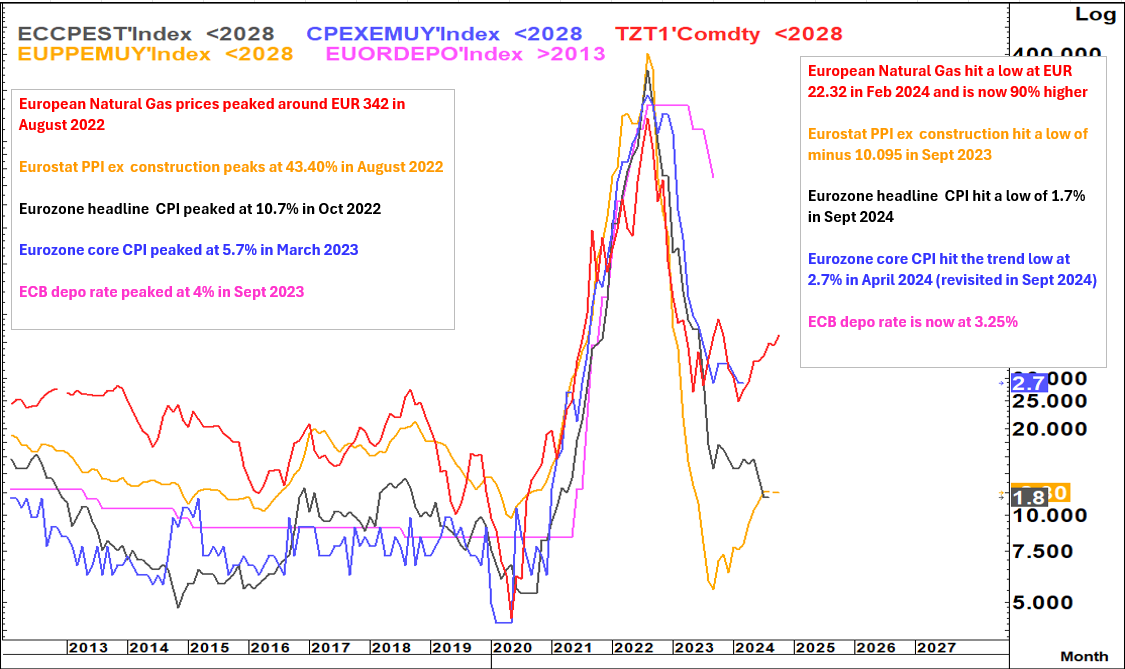

As can be seen from the chart below the rise and fall in inflation on the Eurozone had less to do with Monetary/fiscal policy/demand (Remember the ECB did not even cut rates during Covid as we were already at ZERO and we did not see material Fiscal stimulus) and more to do with Energy/commodity prices i.e. a supply shock.

The chart shows the rise in European natural gas prices and its lagged effect through the various inflation indicators as well as the ECB Deposit facility rate.

European natural gas prices are now 90% up from the February low and PPI has already turned up sharply from its low in Sept 2023 while (for now) both CPI headline and CPI Core rates are at their lows

When Christine L. spoke about the rise in inflation in the coming months followed by a fall away in the months following (particularly in Feb April when we have very strong base effects) it makes total sense.

BUT... the argument for the "technical rise" is far more robust than the argument for the technical fall. That rise will occur even if we print low or ZERO numbers in the coming months (and even more if we print .2 or .3 numbers for example) due to that base effect.

The fall in Feb-April is however dependent on getting low numbers to offset the base effects of the high numbers in the same period last year.

What if those numbers are not a slow as expected or not low at all?

As noted above we have already had a 90% rise in European natural gas prices since February and Oil prices are now up about 10% since early Sept. In recent pieces I have argued that if we close above $72.50 in WTI we could see another 10% or more to the topside with Brent likely following suit

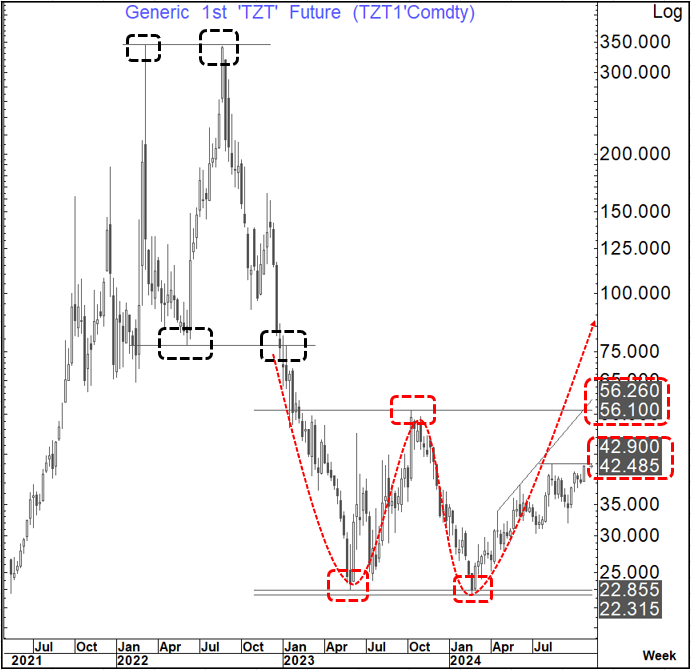

And there is then the chart of European natural Gas.

The sharp fall seen between August 2022 and May 2023 came as a clear double top formed on this chart

As mentioned, we have already rallied 90% off the Feb 2024 lows and are back re-testing the high of this move at EUR 42.90.

IF we see a weekly close above that level it would suggest that we could go back to test the Oct 2023 high (when yields peaked) at EUR 56.10 (about 32% above this level) and IF we were to see a weekly close above that latter level it would complete a double bottom that would suggest as high as EUR90 again (About 112% above present levels and about 300% above the Feb 2024 low.)

Even if this happens it would likely be a supply driven move and should probably be "looked through" by the ECB

But 2008, 2011 and more recently 2022-2023 show us that clearly will not be the case.

The ECB has only one mandate and that is inflation. Right now, in that respect they are using the base effects to allow them to take a much more dovish stance because they clearly know that EU rates are way to high relative to the backdrop.

However, history clearly shows that they do react to supply driven moves following their single mandate in a "single dimensional" fashion.

We need to watch these energy prices like a hawk because if this starts to materialise we will see Christine flip again faster than Simone Biles.

{kind=link}

{kind=link}