Gold is in the ascendancy again but so is Black Gold (Oil) and it looks like both could well head higher still. At the same time the long-term Bloomberg Commodity Index chart is "coming into its own"

Catalysts look to be anything from fiscal stimulus/deregulation to tariffs (front loading of economic activity) to potential supply chain stresses in the World's 5th largest economy (California).

In addition, what we are seeing on Chinese rates with the Chinese 2-year yield reversing sharply higher and the curve flattening could be a sign that the market is starting to believe that the policy measures being taken might yield some results. In that respect Chinese equities have shown a "flicker" of life in recent days.

Gold

Gold has started to recover nicely in recent days and loos set to imminently test good resistance at $2,721 to $2,726. Having seen the recent pullback falter at the 76.4% retracement level that makes $2,726 a valid acceleration point. A break above would target a rapid move to test the all-time high at $2,790.

A break above there would suggest even more gains towards the channel top presently at $2,958.

One of my favourite trades in this respect is still long Gold and short GBP as it still looks like the downtrend in GBPUSD is intact (GBP looks soft across the board). That just hit a marginal new all-time high at GBP 2,221 this morning and the long-term channel top at GBP 2,410 looks a valid target here.

Black Gold (Oil) also has a very positive setup developing (potentially). Having already reached the first two double bottom targets of $76 and $78.50 to $79 respectively it is now on the cusp of completing a much more material double bottom at $78.50. The equivalent pivot on Brent Crude is at $81.16

A weekly close through $78.50 on WTI here would target extended gains towards $90.

For another day BUT.....IF we saw a decisive break over $95 that would complete an even bigger double and suggest we could go back to test the high range seen 2022 at $124 to $130. It is worth noting that during that surge to $130 in Q1, 2022 it was accompanied by a coincident rise in long-term US yields. Then, obviously, the central catalyst was very different in that we had the Russian invasion of Ukraine in February 2022 but the trend higher in Oil and yields was already taking place before that "fuelled" the flames.

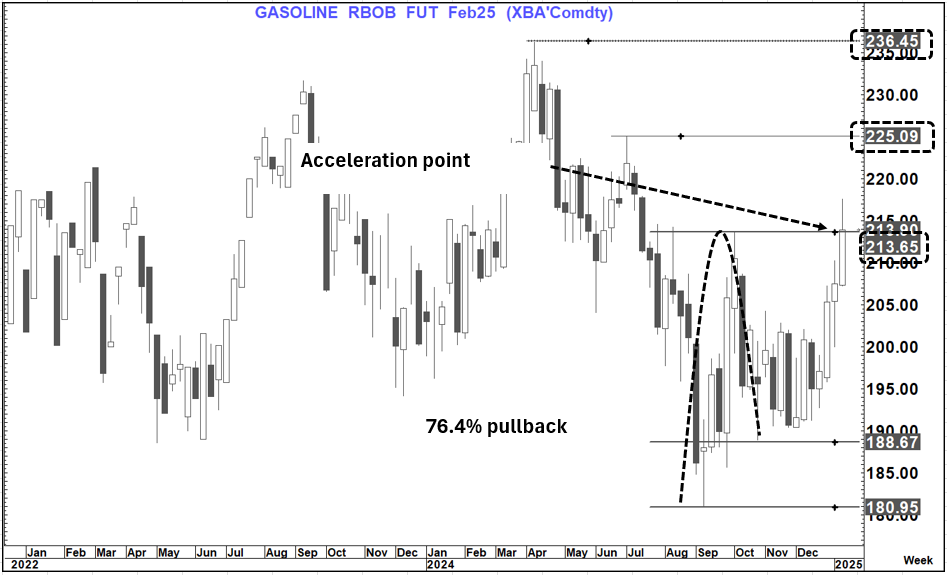

This not surprisingly is also feeding back into Gasoline.

Following a 76.4% pullback Gasoline is now testing the pivot point at $2.1365. A weekly close above would suggest further gains (impulsive) to at least $2.25 and possibly the 2024 highs at $2.365. Above there the 2022 highs stand at $2.4250

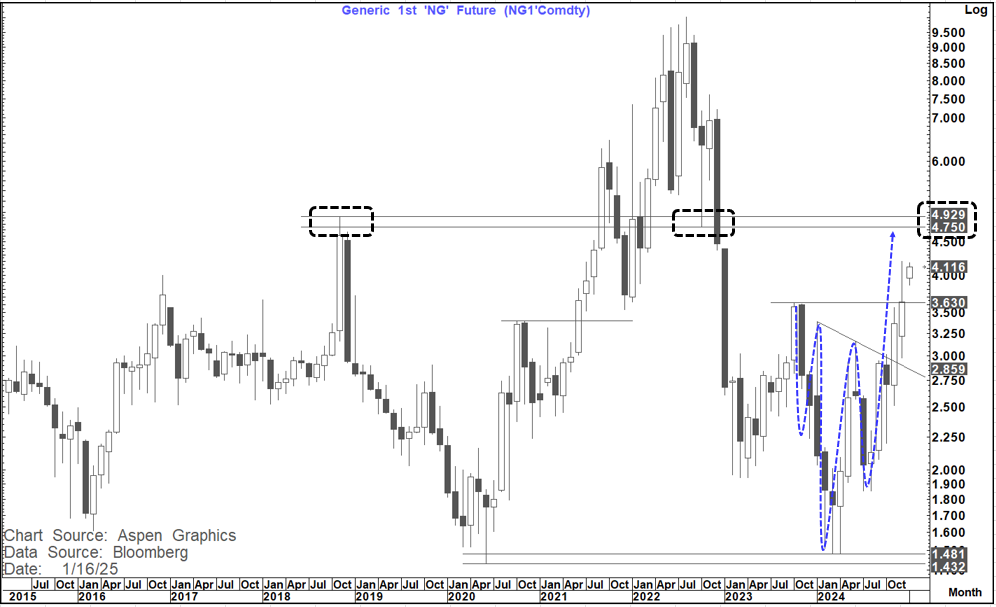

Natural gas is also interesting

We have completed an inverted head and shoulders off levels similar to the low in 2020 that targets around $4.75 on a nominal move basis. this is also an area that has some good horizontal resistance.

A move above the $4.75-$4.92 area would open up the way for more material gains. In 2022 that was above $10 but again we had the "Ukraine" effect

If we targeted the head and shoulders move on a percentage change basis that would suggest more like $6.50 as a target, which is pretty much where we accelerated to in October 2021 during the last bull market.

Copper is also trading well here.

It has just completed a clear double bottom that targets a move towards $456 (which is not that far away now). This is similar to what we saw in March 2024 that ultimately saw it move a lot higher than the target.

Above $456 would open up the possibility of a test of the Sept. 2024 high at $479 and that is a pivotal level. A decisiive break of that level, if seen, would suggest further material gains targeting $560- also where the trendline off the last two highs in Jan 2023 and May 2024 comes in. Interim resistance is met at the May 2024 high at $520

The Bloomberg Industrial metals index is also rising and could post a bullish outside month IF we close over 147.75 (last 145.93)

Not surprisingly the Bloomberg industrial metals index looks just like Gold.

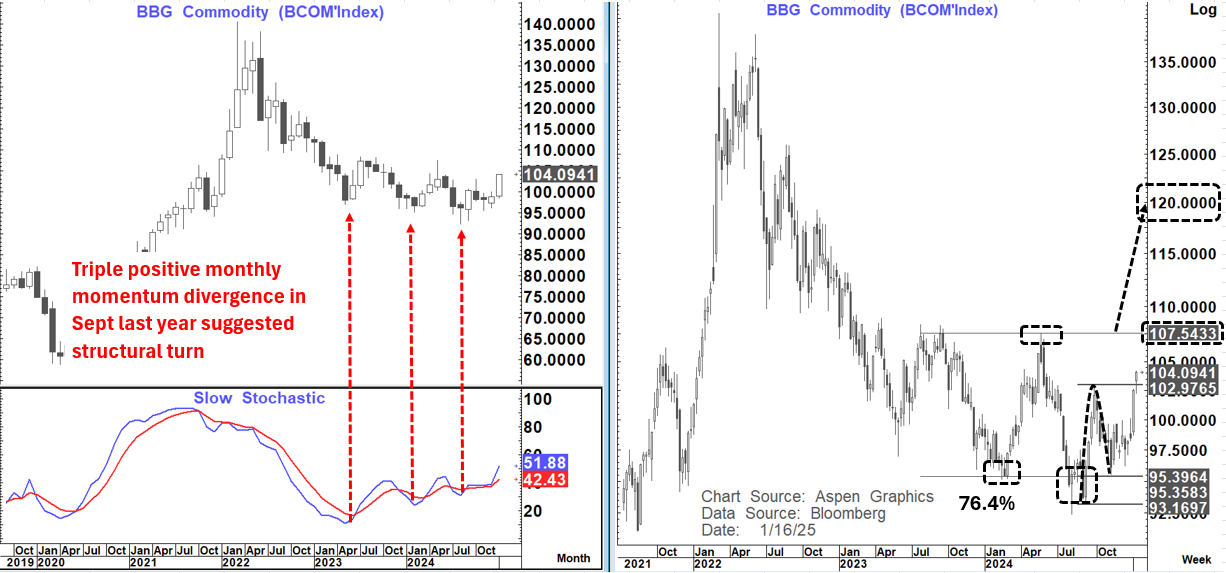

This all takes us to a chart put out in Q3 last year- The Bloomberg Commodity index.

In September we posted triple positive triple momentum divergence on the monthly chart which suggested much higher levels over time. That looks to be materialising now as we have just broken the 76.4% pivot of the recent correction lower and accelerated. A test of the 107.50+ area seen in May last year now looks likely and a break above, if seen, opens up the way for extended gains towards 120.

All of the above suggests we may be on the cusp of quite a bullish move higher on commodities. IF so how does that feed to other markets?

It should be bearish Fixed income. However, with the Fed "trapped" into inaction here (for the near term at least- despite Waller's comments today) we have already had our move on the 2-year yield and should not be able to sustain above 4.5% or below 4.25% while that narrative of Fed going nowhere is sustained. Only a belief that the Fed is likely to raise rates next time would dramatically change that picture. (Or an unlikely cut in March)

The USD should be a beneficiary of higher yields in particular if that also yields wider spreads with Europe and Japan. I still favour a weak GBP as their rise in yields is coming for "bad" reasons and risks a stagflation backdrop as they do not have the same buffers on mortgages etc. that the US has.

Equities are a work in progress to the extent that this rise in yields is viewed against the backdrop of a robust economy- that should naturally benefit equities. However, there is a danger that we are pricing in all the good news about the market friendliness of the next administration and also seeing some pre tariff front loading by companies. If so, then further down the line there could be a danger that higher yields and higher commodity prices after a front-loading economic effect could create an early 2025 "sugar-rush" to be followed by a later 2025 "headache"- but again that is a work in progress.

For now, the most important message here is that the picture for commodities, if it materialises as expected, could see much higher levels in Q1 and that could feedback into both higher yields and a higher USD. After that everything is likely a "work in progress"