In this piece I patch together the highlights of Six pieces written between 21 and 29 Oct, with a few new comments. The message is clear. There is an increasing danger that US Yields (and possibly also Europe/UK etc getting dragged in the same direction ) are set to move materially higher than where we are today and likely sooner rather than later

We did get some expected pullback in this move in recent days, but it is already looking like that correction lower in yields may have already run its course, And, despite obvious event risk in the coming days it looks like yields are once again setting up to move higher again.

On October 21st I put out a piece titled

Parting is such sweet sorrow (all blue titles are links to the prior article)

In this piece I noted that what we were seeing in yields and in particular on the 30-year yield chart was giving me concerns and inclining me to part ways with the 2007 analog that I had followed for the prior year from October 2007.

This suggested that the move lower in yields subsequently seen in 2007 was now looking less likely.

Then on 22 October I put out a piece titled

Déjà vu Or Different This Time

In this piece I noted that while we saw yields peak and turn lower on 21 Oct 2021, 21 Oct 2022 and 23 Oct 2023 it was looking different this time.

Then on 23 October I put out a piece titled

In this piece I stated that IF we saw a weekly close above 4.09%-4.13% in the US 2-year yield then a quick move towards 4.40-4.42% would be a danger

Then on 26 Oct, I put out a piece titled

Here I noted what I believed to be a credible path towards that 4.40% to 4.42% target with particular focus on

Geopolitics

The employment report

The Election

The Fed meeting.

Then on 29 Oct, I put out two pieces titled

Both of these pieces focused on JOLTS and the very real danger that we get a decent employment number on Friday and trigger one of the "pieces of the puzzle" mention above (The others being the election and the Fed itself)

Since then, I had expressed caution that we could see some consolidation/correction in yields short-term as risk got trimmed ahead of these events.

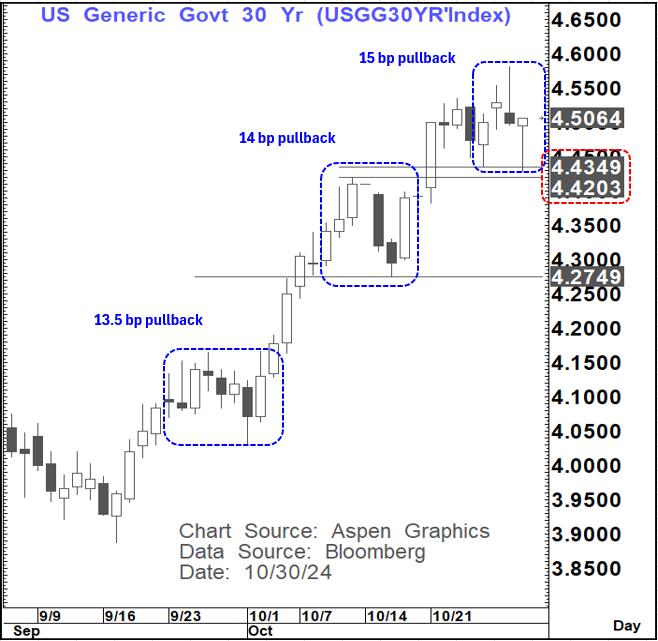

We have seen some back up in yields with the 2-year yield going back to 4.07%, the 10 -year yield to 4.20% and the 30-year yield back to 4.4290%

In particular today I was focused on the 30-year yield and very good support (yield) at 4.42% and 4.435%. A move below there would have suggested an even deeper correction towards 4.275%.

But it did not break that range and bounced strongly

And what about that 2-year yield chart

We obviously still have the employment report and the weekly close to come but it is looking like we are now sustaining this break above that 4.09%-4.13% (probably more 4.12% to be honest) range.

As previously articulated, that would almost certainly have implications for the markets view of the Fed path and possibly even for the Fed's own view

Now for an extra kicker- What if that 4.40-4.42% range were to give way. That would open up a danger of a Jan=April 'esque 2024 move (possibly towards 4.70%) which back then was accompanied by a very sharp repricing lower of the expectations for Fed cuts.

In fact, a level like that would strongly suggest a Fed going back to the sidelines and pausing in a 1998'esque fashion.

So, it looks like the upward move in yields is firmly back on track and potentially set to accelerate as we head through the "event risks" of the coming days.