US Yields pushed higher as expected on the back of the "Unbelievable" (literally) data on Friday but of course we have another pre-Fed number to come. I posted some thoughts in that respect in my weekend diary piece Diary Week 62: One Of These Things Is Not Like The Other

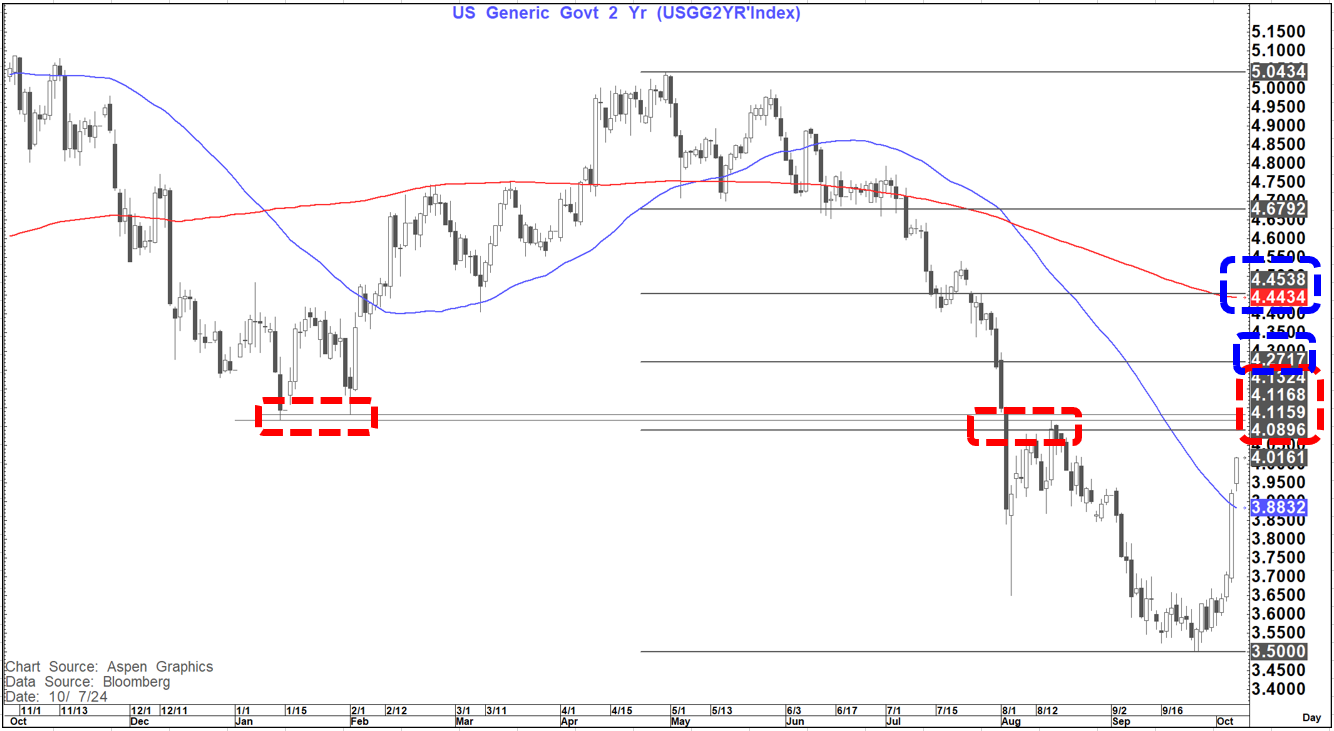

US 2-year yield: Has pushed above 4% overnight and may well be set to extend towards very pivotal levels around 4.09%-4.13%. (In line with the 2007 analog that would likely be within the next week or so).

However, as I always say- "History does not repeat but it does rhyme". In that respect we have to entertain the idea that we could go even further.

IF we break that 4.09% -4.13% range the next target would be 4.27% (50% of the fall) and then 4.44%-4.45% (61.8% of the fall and the 200-day MA .)

That is not my base case scenario at this point but the other phrase I often use is that "The only thing that is unthinkable in these markets is that anything is unthinkable"

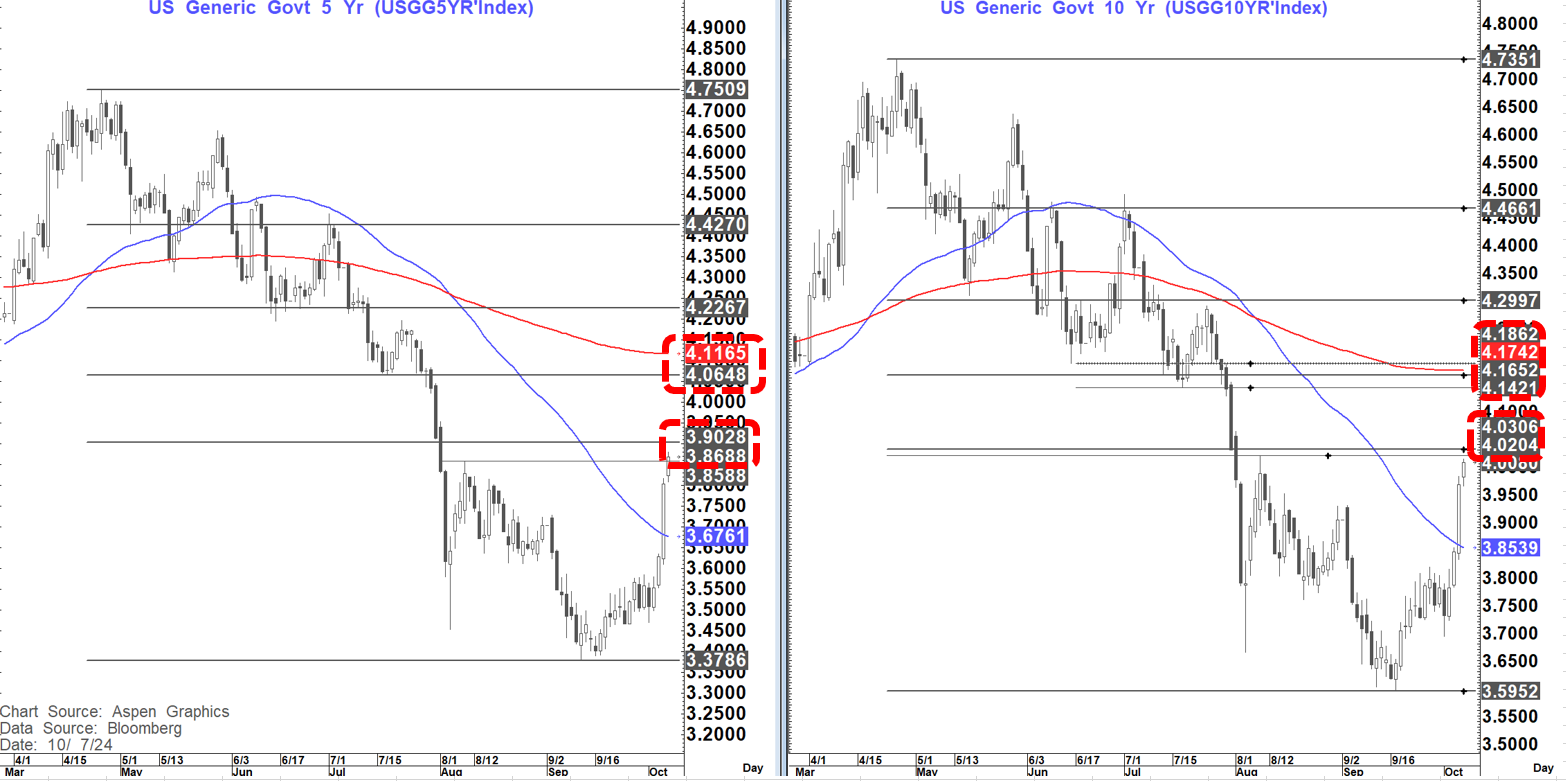

On the US-5year yield the first good level is already being tested at 3.87%to 3.90%. Above here next good resistance is at 4.06% to 4.12%

On the US 10-year yield we are also testing 4.02% to 4.03% resistance. A break above here and 4.14% to 4.19% could come into play

What about the curves?

After holding the initial 200-week MA target the 2's 5's curve has flattened sharply as yields have moved higher. Initial trend line support comes in at minus 17 but a re-test of the pivotal area at minus 19 to minus 21 looks likely.

On the 2's 10's curve rising trend line support at +6 bp's has given way as has the initial +1.5 bp's target. Main support now is met at minus 11 to minus 16 bp's

Commodities

WTI and Brent both posted their first bullish outside weeks since February this year from near the trend low and significant support levels. Despite no new material developments over the weekend (yet) Oil is clearly trading differently this time with gains continuing to materialise way past Geopolitical headlines this time.

At minimum it looks like WTI can head to $80+ and Brent to $82+ but there is a real danger that even higher levels can be seen. Further levels are met on WTI around $84 and on brent around $87 to $88

Very big levels come in around $95 on WTI and $97.70 on Brent and it is NOT inconceivable that we could head there.

Up until now Oil was a missing link to the 2007 scenario when it surged in Q4- That may no longer be the case.

Initially the Oil move likely further fuels the yield moves but this is not a demand driven rally. Over time, if this rally continues, it likely serves to be more of an economic drag causing a quandary for the likes of the ECB who only have an inflation mandate.

However, as we saw in 2008 and 2011, when policymakers do not recognize the cause and effect of the move they make policy mistakes. This move higher, if it comes, should not induce a change in monetary policy.

Gold and bitcoin while choppy still look to have a bullish setup and I still expect that moves to $3,000 and $75kto $85k respectively can be seen

On FX we should expect further USD strength to materialise if these yields continue to move higher and curves flatten

Some likely targets to watch are:

USDJPY: 151.09 (200-day MA) and possibly 153+ (Inverted head and shoulders target). First good resistance is met at 149.39

EURUSD: Double top below 1.10 suggest 1.08. Interim support is met at 1.0948 and then 1.0875 (200-day MA)

USD-index (DXY) looks likely to head towards 103.65-103.75

Equity Markets

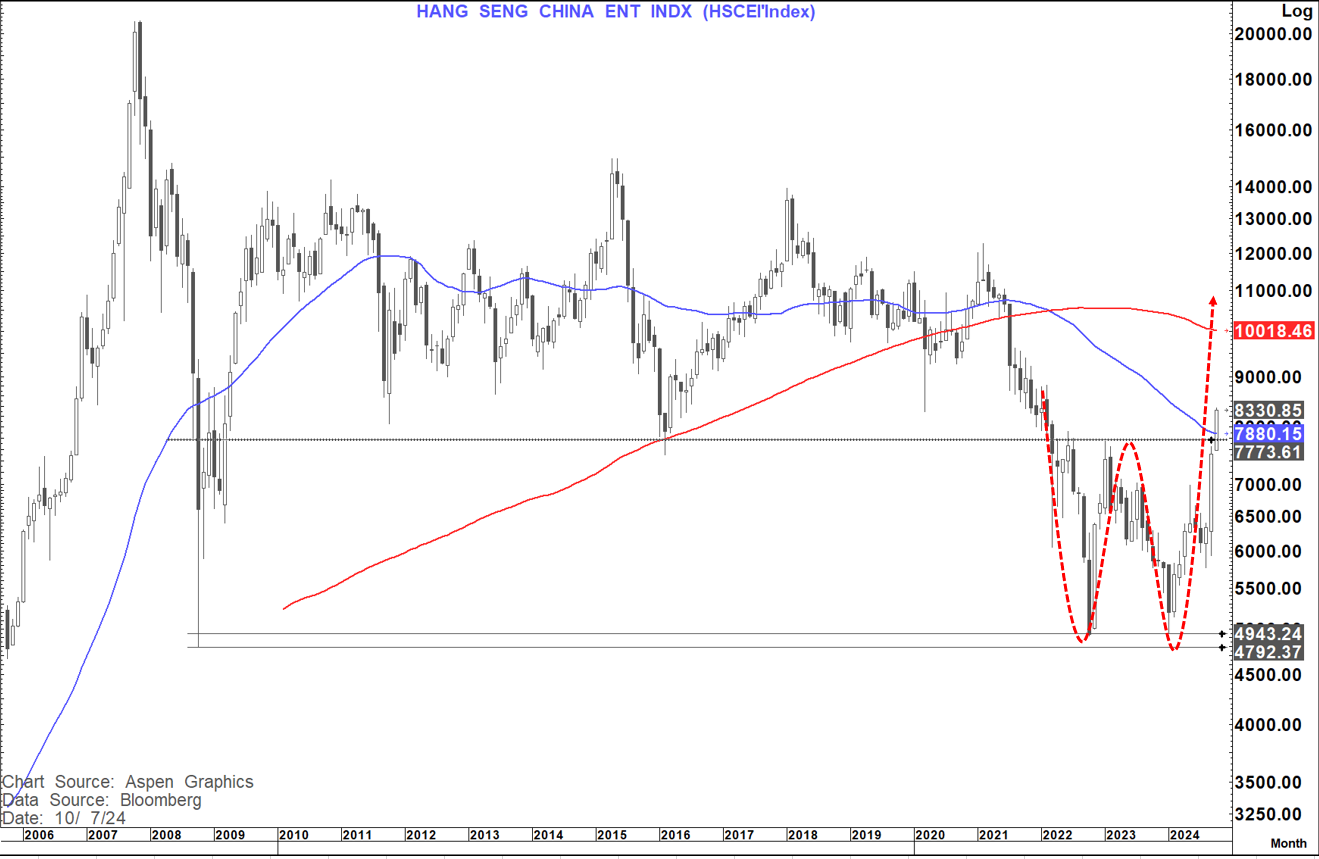

Chinese Equity markets are "On a tear" again. Technically the "Poster Child" to me looks to be the HSCEI index

having bounced off almost identical levels to the turn in October 2008 it has now completed a break of the 55-month moving average and a double bottom neckline. The 200-month moving average stands at 10,018 but the double bottom suggests a move as high as 10,600+.

On US equity markets while we are moving into the timeframe where we saw them turn in 2007 there is no indication as yet that a similar turn is materialising. A decisive weekly close on the S&P back below the July high, if seen, would track closely how we turned in 2007.

That is still quite a bit below her at 5,670. However, at least for now on equities the trend is your friend.

{kind=link}

{kind=link}

{kind=link}

{kind=link}