I have incessantly commented over the years that my Financial Bible is the US 2's 5's curve which has regularly been a good leading indicator of curve movements off pivotal points. In addition, the US 5-year yield has often, in itself, been a good signaling indicator for yield direction as a whole.

Both of these charts have interesting setups right now.

US 2's 5's curve

The big break on the way up in this curve was above minus 19 basis points which suggested a move as high as +30 bp's (high so far was +25 bp's)

As Fed expectations have been pared back, we hit a high in January that was accompanied by triple negative momentum divergence on the weekly chart (High, higher high and higher high in yield while seeing a high, lower high, lower high in momentum)

That started the move lower to where we are today.

On that last leg up we pushed higher once we broke above good resistance at +6.4 bp's and on the way down that level was initially tested and held on Monday this week bouncing back up to +12.7 bp's .

We have since started to fall again and have moved below +6.4 bp's again. IF we sustain that on a weekly close (Employment data tomorrow looks key in this regard) the suggestion is that we could correct even deeper and possibly move into inversion towards minus 12 to minus 14 bp's .

That, in my view would be a big deal and the first move back into inversion from strongly positive levels since July 2022.

The sharp fall in the Jobs plentiful/Jobs hard to get ratio followed by the subsequent sharp fall in JOLTS suggests the danger of a downside miss on Friday (possibly by as much as 100k). However, there are a number of top market forecasters looking for numbers in the 250k to 300k range and as we know any one number can come in anywhere.

So given the sharp move we have already seen in both the curve and yield direction i recognise it is hard to go into this number with an aggressive long F.I. or short curve trade. However, if we do get a soft number (or we see another sharp revision down in prior numbers suggesting that the BLS numbers are really BS numbers) then this move would look very much on the cards.

I believe that a move back to inversion here, if seen, would be a big wakeup call that all is not as rosy as it seems or that the market is staring to buy into the idea that this administration is serious about spending cuts. Following Bessent's comments yesterday the big beneficiary of both these scenarios is likely the longer end of the curve with associated further flattening likely

What about the yields themselves

Right now, it is hard for the 2-year yield to sustain any material break below 4.255 or above 4.5% unless and until the market starts to believe that another Fed move (either way) is imminent. Even one poor NFP number (unless it is disastrous) would be unlikely to move that needle so likely what the 5-year yield does is more important for this curve (for now at least)

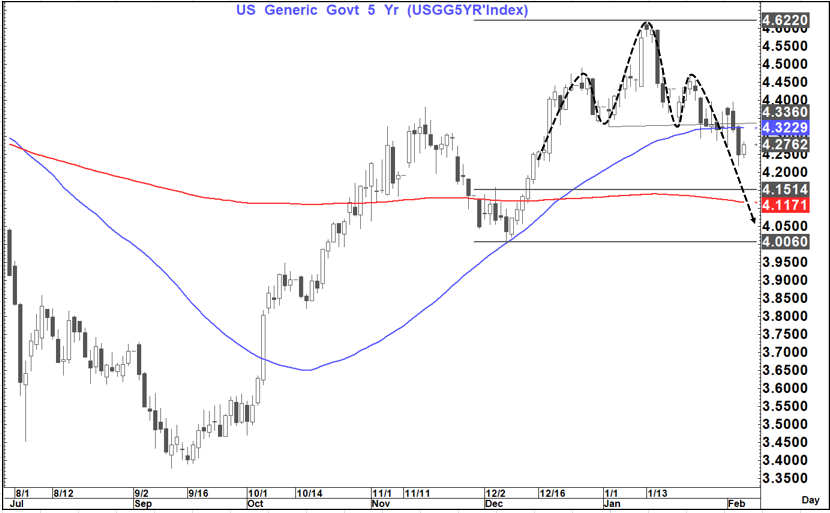

US 5-year yield.

We have completed both a head and shoulders top and a break of the 55-Day MA that suggests a move towards at least 4.12% and possibly 4.03%.

Good horizontal support also stands at 4.01%

A weekly close below this 4.32-4.34% range , if seen, would strongly support this potential move lower and likely flattening of the curve. A close above, if seen, would likely temper that potential.

Even if we get this move lower in the curve, it is not clear that this is a trend turn, and it is likely that the minus 12 to minus 14 area could be a platform to move higher again. Remember in 2019 (July 31) the Fed cut rates after this curve re-inverted (17 July) and they cut again on sept 18 after the curve inverted 15 bp's (28 Aug)

In early July 2019 the Employment release for June saw NFP print 160k (expected 224k) and the unemployment rate rise 1/10th. In early August NFP beat slightly but was offset by a prior downward revision. The unemployment rate was revised down 1/10th for the prior month but then came out 1/10th higher than expected for the July number.

The Fed has been very clear that they neither need or desire any further softness in the labor market so that means it has once again risen in importance for them and needs to be watched. This is especially true as signs suggest that inflation is being well behaved at the moment and concerns re tariffs and the budget have to, if anything, also been alleviated by developments.

Bottom line the setup looks good for lower yields and a lower curve...BUT...right now this market is dysfunctional and reactive to any new headline or employment print. having moved so far therefore there is very little positive risk/reward in going into the numbers heavily exposed to these trades only to get "annihilated" if we get a strong print.

Rather wait to see if the numbers disappoint and if they do look for good levels to re-engage in the trade.