Last week was one very choppy week and next week is unlikely to be any easier with the "Elephant In The Room" being the election but of course we also have the Fed meeting.

After the employment data is seems very likely that the Fed will ease next week. There is virtually no chance of a 50-basis point cut but the expected 25 looks very likely, if not a certainty.

Without the cover of a strong employment report on Friday it would be very hard for the Fed not to look political by not easing if we got a "Trump victory/ Red Sweep", so, a 25 bp's cut seems a given.

However, if we did get that political outcome, it might temper their enthusiasm to strongly guide for another move in December.

For the past 4- years the direction of rates has been driven by inflation (transitory then not) and more recently employment. In UK, Europe and Japan, inflation has been a more central focus.

As a consequence, the views, guidance and actions of the Central banks have driven markets

Could that be changing?

We have seen recently in both the US and the UK that fiscal responsibility (or likely lack thereof) has become an increasing driver in directional and curve moves.

In the US it has been labeled the "Trump Trade" but the reality is that fiscal responsibility has totally disappeared on both sides of the aisle. For a substantial part of my career this has tended to be a "nothing burger".

But I am beginning to feel that this is changing as we get the combination of an outsized deficit and higher overall funding costs.

As I have previously mentioned the US now has a national debt of over $35.8 trillion. In 2006 that number had grown over the life of the USA (1776-2006- 230 years) to $8.5 trillion.

In the subsequent 18 years we have "tacked on" a further $27.3 trillion.

Since 2019 the US economy has grown in size from $21.5 trillion to $29.2 trillion ($7.7 trillion). During the same period the National Debt has gone from $22.7 trillion to $35.8 trillion (+$13.1 trillion)

We now have a debt of $106k for every citizen and $272k for every taxpayer. (This liability is only the national debt. It does not include unfunded liabilities which ae estimated around $102 trillion)

In fiscal 2024 the US Government passed the $1 trillion mark in gross interest payments on US debt for the first time. While the 2 biggest expenditures in the US budget are Social Security (22%) and Health (14%) at 13%, net interest has now caught up to Medicare (13%) and national Defense (13%) and continues to grow.

And of course, in the UK last week we had a "mini Truss" event on the back of the UK budget.

Is the market finally realising that there is little chance that Central banks have a "Paul Volcker" 'esque appetite to do the right thing and that they will "fold like a cheap suit" as soon as the "pain" is felt.

Politics and populism now seem to drive so many decisions in our World.

If central banks are not prepared to counter the Fiscal irresponsibility, then who is?

The markets?

I begin to think that outside of politics and geopolitics and economics and inflation and employment etc. etc. etc that maybe this could become the defining driver for yields as we move into and through 2025

Short end yields will still remain anchored to policy rates so 2's are unlikely to be the leader in this move (Unless at some point the market starts to think that the Fed may hike again) . More likely that will be 5's 10's and 30's with significant steepening of the curves as a consequence.

We always have to ask ourselves in markets where is the "Achilles heel" that could blow things up?

Banking, Housing, MBS, equity markets, Policy moves etc. etc.

Maybe, just maybe, in this cycle it turns out the Government Fiscal irresponsibility is finally the "Chicken That Comes Home To Roost"

As I said above, in the medium-term I think this is an issue no matter what composition of Government we get on Tuesday (or some shortish time thereafter)

However, in the near term the market defines this more as the "Trump Trade".

So, what might markets do next week- which right now is likely a bigger focus for participants.

I think there are 3 scenarios but 2 outcomes

Trump victory

Kamala victory or uncertain result

YIELDS

IF, Tuesday is a Trump victory then:

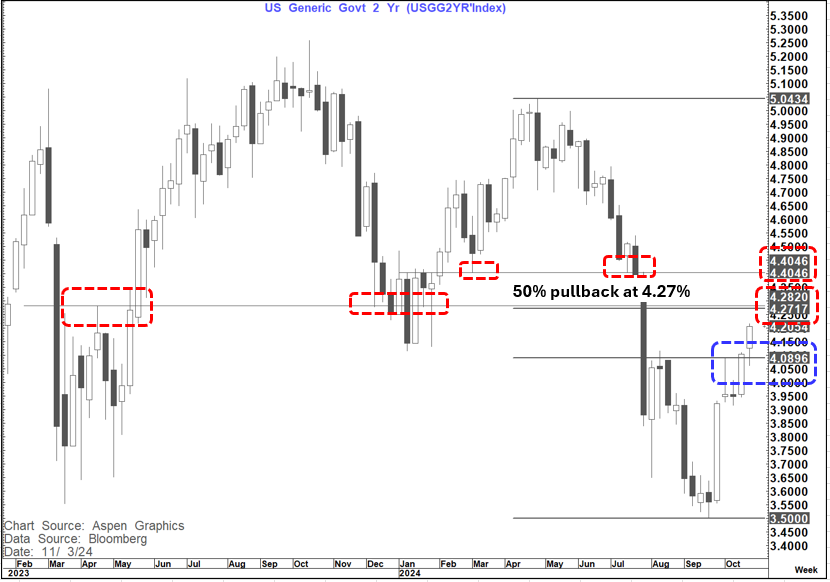

We likely pop higher again in yields initially. On the US 2-year yield they would open up for a move towards 4.27-4.28% and above there to 4.40%-4.42%. But, absent a Red Sweep we are likely then subject to a "sell the rumour, buy the fact" outcome-especially if we headed towards 4.40%. It is the first week in November and people will likely be quick to monetise any windfall profits.

IF the outcome looks indecisive or a Kamala victory then the danger would be a decent fall in yields with the 2-year yield potentially shifting back towards 4.09% again

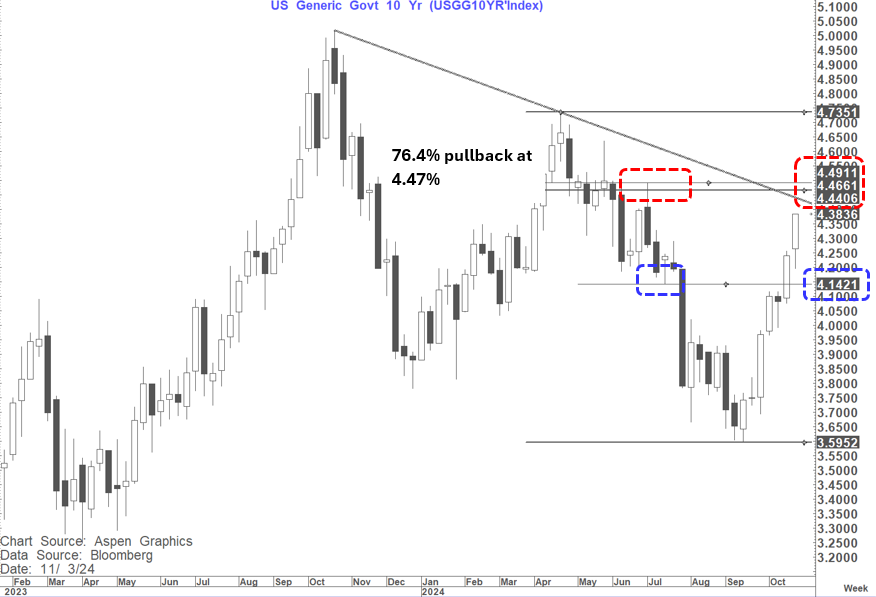

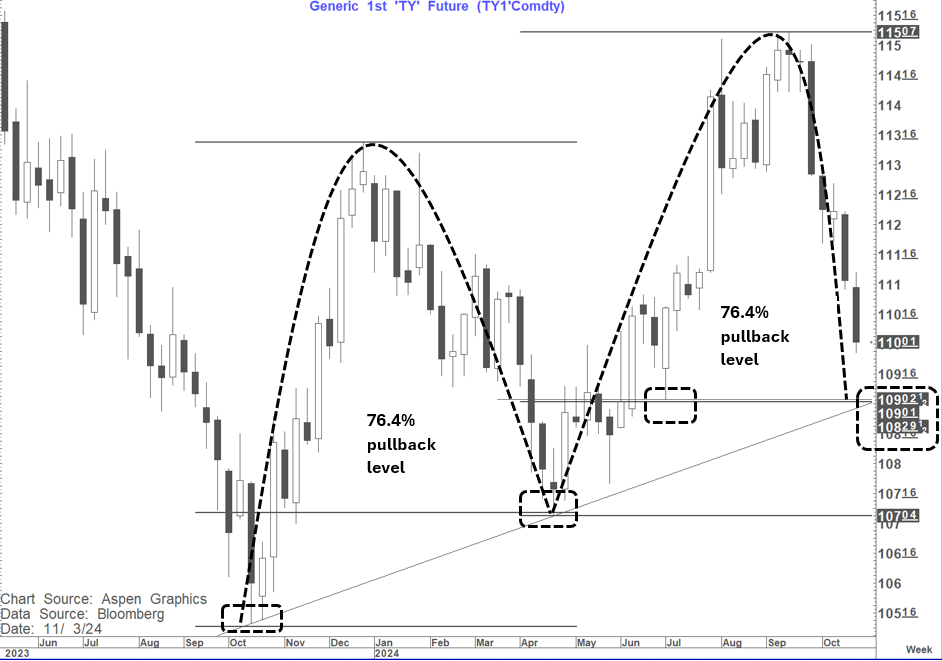

Trump victory: On the 10-year yield we should quickly see 4.44-4.49% and possibly 4.53%. Above 4.53% and all of a sudden 4.74% comes into view but that is probably not likely as an initial move. The 4.53% level actually comes not off the chart itself but from an extrapolation on pivotal levels on the Ty1 chart

Kamala victory/ indecisive: 10's towards 4.14%

On TY1 we have a hugely pivotal area around 109.

EQUITIES

Equities will also likely bounce initially on a Trump victory but the up moves here look tired now and we have rallied into the election this time rather than fallen as we did in 2016 and 2020 so I am not sure that this move would be sustained either. The overall technical picture on equities definitely suggests caution. On Friday we posted a bearish outside week on the SOX index and technology stocks in general could be susceptible to higher yields.

On a Kamala victory or indecisive then equities fall immediately

FX

On a Trump victory the USD will go bid as a reaction to the pop in yields with USDJPY very susceptible as it seems a lot of people bought JPY last week against the USD and crosses on the back of Ueda's comments. But on the tariff side Europe, Canada and Mexico may also wobble.

On a Kamala victory or indecisive the USD likely gets hit as yields fall

BITCOIN/GOLD

On a Trump victory Bitcoin likely bounces sharply but Gold more "nuanced" Do not know if it would initially like the higher yields and bid USD

On a Kamala victory or indecisive Bitcoin gets crushed.

As an aside it is interesting as I write to see how Bitcoin is trading right now. It already looks like the IOWA polls have pushed the "indecisive" narrative a bit more. I wonder therefore if we see Equities and the USD under a little pressure at the open tonight and yields fall back somewhat from the highs at the Friday close). As it is an "owned" position I think Gold as well as any other "owned" positions could also get squeezed lower tonight.

All the above are just some thoughts and obviously Election night is likely to be very fluid.

More importantly, there will be a point where the result becomes obvious (that may or may not be quickly) and hopefully the market dynamics will then be better informed and the direction into year-end clearer.

Before that happens, I think the most important thing is to be positioned for that point. Overtrading in the next few days is quite likely to be a painful experience no matter what your market view as headlines swing us sharply in both directions.