The narrative of the day in recent times has been to question whether this is the end of US Exceptionalism?

As Winston Churchill is reputed to have said " America does the right thing once it exhausts all other possibilities".

So, while exceptionalism is not a word I would likely use for the US Government or the US fiscal approach (Particularly from the GFC onwards) it is still a very valid word when it comes to the abundance of riches the US enjoys in terms of major corporations, technological innovation, productivity, and natural resources.

This is certainly a challenging time, and, in that respect, I should mention a very good read I have just finished titled "Peddling Protectionism" by Douglas Irwin.***

I so often "Trot out the phrase" attributed to Mark Twain that "History does not repeat but it does rhyme". I think this book clearly has elements that "rhyme" with today.

The US will get through this and likely come out stronger as it has done in the past. That is not to say that we will not have difficult times ahead. The backdrop and various market charts suggest a danger of tough times ahead but betting against America long-term has not been a fruitful exercise.

What about short-term?

Much has been touted about recent European outperformance and in particular the landmark decision in Germany regarding constitutional and budget reform. This will loosen borrowing limits for defense spending and foreign aid and earmark EUR500 billion for infrastructure borrowing.

Here's the thing.

Germany has a debt to GDP of around 63% which provides plenty of space in today's world for expansion. What about the other major EU economies?

Germany: GDP 4.4 trillion. Debt to GDP of 63% (Anticipated to move as high as 90% over the next decade or around EUR 120 billion a year growth)

France: GDP of EUR 2.8 trillion. Debt to GDP of 111%

Italy: GDP of EUR 2.09 trillion. Debt to GDP of 135%

Spain: GDP of EUR 1.46 trillion. Debt to GDP of 104%

Netherlands: GDP of EUR1 trillion. Debt to GDP 0f 47%

Poland: GDP of EUR 735mm. Debt to GDP of 50%

The German move obviously has notable short-term impact, but it is far from clear that this will have a more medium-term economic effect. Germany has not grown effectively since the 4th quarter of 2022. Added to this is that fact the Germany (and the EU) is a very export driven growth model that at the moment has not one but 2 Achilles heels .

Slow China growth

The onset of US tariffs. While tariffs (especially tit-for-tat) tariffs can impede economic growth on both sides it is the "net exporter" that is likely to suffer more.

However there also has to be a question mark about how much the other big 3 (France, Italy and Spain) can engage in the same level of debt expansion given their already elevated debt to GDP ratios above 100%.

Additionally in just 5 trading days into March 6th the 10-year yields surged in these countries: France +53 bp's ; Italy +50 bp's and Spain +52 bps while at the same time the US 10-year yield moved up 10-15 bp's. Given the close relationship to yield spreads this provided a boost to the EURO but on a more negative dynamic than prior in that the spread narrowed on rising European yields not falling US yields.

The EURO did of course rally also as did European equity markets.

Is this sustainable or just "Europe's 15 minutes of Exceptionalism"?

Looking at the charts below I am more inclined towards the latter than the former. Let's us look at 3 charts in particular.

1. BUND

Here we see clear suggestions on the weekly chart that the BUND could be turning.

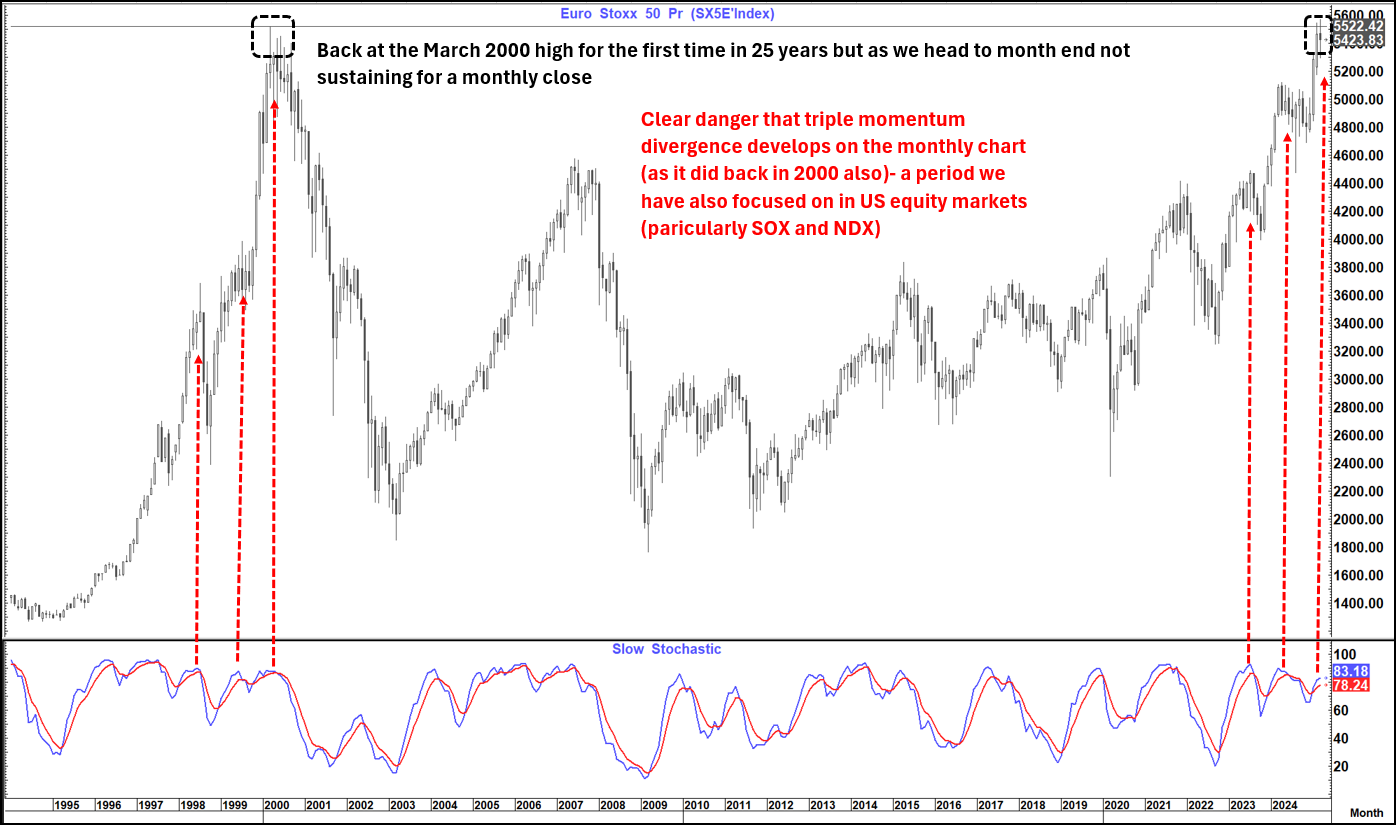

2. SX5E (Eurostoxx 50 Index)

As we re-test the March 2000 all-time highs in this index (for the first time in 25 years) the chart below suggests some reason for caution. As a side note we have been closely focused on similarities to the way the SOX and NDX are trading today and how they traded into the Dot-Come bubble of 2000.

Then the Fed retained its concerns on inflation thereby not cutting rates until Jan 2001 after the NDX had already fallen 56% and the SPX close to bear market territory at down 19.25% (That would equate to a move below 5,000 this time)

Clearly at this point in the move there is no Fed of Trump put on the equity market.

Also (as an aside) the ultimate turn and fall in the NDX in 2000 was most similar to the turn and fall seen in the DJIA in 1929-2932- the only 2 times a major US market has fallen over 80%

3. EURUSD

I have noted how similar the price action in EURUSD has been to that seen in 2022 as can be seen in the chart below.

This chart clearly suggested a 2-week pause/correction down towards 1.07 before higher again.

However, are we seeing some subtle differences already?

Back then we had already started to bounce in week 2 whereas last week we came dangerously close to posting a bearish outside week at the trend high (Needed a close below 1.0805 and closed at 1.0813)

In addition, EURUSD also completed a double top of just below the 76.4% retracement level (1.0961) that suggests a move to at least 1.0695-1.0700. That level would not be inconsistent with 2022 but below it would be.

Bottom line any extension below that area would call the comparison into question and suggest a danger of even lower levels and possibly a turn on EURUSD.

*** With regard to the book above some quick observations***

-It relates to the Smoot Hawley Tariff act enacted over 1929- 1930 after a republican sweep of the presidency, house and senate in 1928. At this point the US economy was in very good shape and unemployment stood at 3%

- Back then Congress and senate had control over tariffs, but the US President had the power of Veto and the process dragged on all the way into June 1930 after first being proposed in April-May 1929.

- It brought down a Canadian prime minister (and in fact Government) in favour of a more adversarial conservative Govt. Mark Carney will not make that mistake and is already talking tough improving the General election prospects of the liberal party (immeasurably). He has just called a general election for April 28th. However back then Canada suffered mightily in the tariff process and a lot of talk grew of reciprocal trade agreements (particularly as related to the old Bristish empire) as a result.

-Tariffs in themselves may or may not be inflationary but reciprocal tariffs as we saw then (tit-for-tat) depressed growth and thereby became massively deflationary

- A strong trade partner and good neighbour to the south saw the Government fall as a result of these tariffs only to be replaced by a government much less friendly with ultimately lasting repercussions- No, not Mexico- Cuba.

I have talked on a number of occasions about now similar the chart on the SOX and also the NDX today are to what we saw in Sept-Oct 2000 so I will leave you with another chart

This is a comparison of the 2000-2002 NDX and the 1929-1932 DJIA paths.

In 1929 we had a strong economic back drop which faded rapidly. While full cause and effect cannot be conclusively attributed a combination of Tariffs, a stock market crash and an intransigent Fed all contributed to this backdrop

in 2000 we had a Fed resistant to cut on inflation fears. This followed easing in 1998 on the back of a contagion- Financial not medical. We had LTCM, the Russia default, the Asian crisis and the Mexico crisis.

As a consequence, as the equity market turned as the DotCom bubble deflated, the Fed (again unlike 1987 nut like 1929) was "intransigent" and waited until Jan 2001 to move as the stock market fall intensified and the feedback loop into the real economy materialised

Today we have a tariff scenario. today we have a Fed that will not be inclined to buckle for the Stock market given their confusion about conflicting economic /inflation signals. Today added to the frame is Geopolitical uncertainty and a "disruptor" in the white house.

This is not 1929. This is not 1987. This is not 2000....BUT it sure is a "Mark Twain" triple play

{kind=link}

{kind=link}

{kind=link}

{kind=link}