The analogs that have served us well for most of this year (1990/2000 and in particular 2007) are still in play (particularly 2007) but we are getting to a point where the optimal scenario (price action and backdrop having similarities to the historical period) is reaching an inflection point.

The 1990 dynamic (mainly with a Japan backdrop) where Japan raised rates aggressively while the US eased is now diverging somewhat. Japan is clearly "balking" at the idea of an aggressive tightening cycle while the Fed is expressing cautionary notes about the speed of easing (although 2 more 25 bp cuts this year is still my base case). Recent rhetoric on inflation from the Fed clearly shows that 25 bps is very much on the table for November.

2000 still resonates somewhat (especially if the Fed backs away) but more in terms of the equity market and the NASDAQ/SOX in particular.

But the reality is that at this point both in terms of the equity market and the bond market (in particular the 2-year yield) we are tracking much closer to the 2007 path.

Without trying to sound like a "conspiracy theorist" the 785k seasonally adjusted Government jobs created in Sept defies all bounds of credulity (and directly and dramatically changed the unemployment rate) which means that the release on 01 November retains a high level of importance.

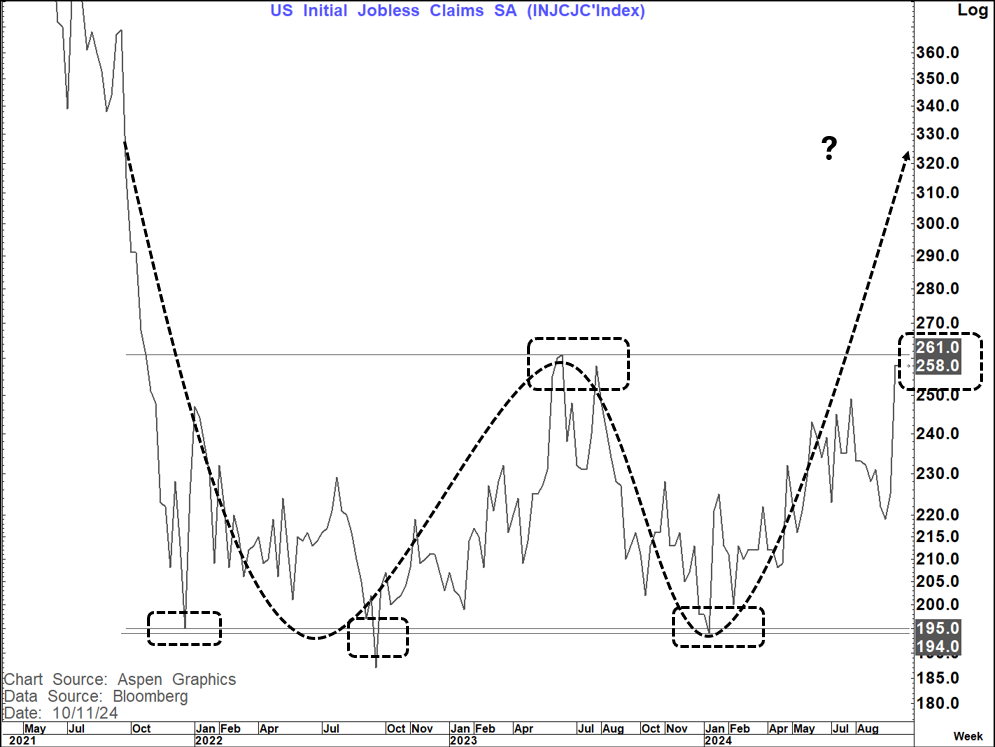

We also need to watch for the next few initial claims releases. At best the rise last week had around a 30% "hurricane" factor to it and was very broad based. We need to see IF that number drops back or if something else is going on. A move above the 2023 peak at 261k , if seen, would definitely raise some questions.

We also have a number of housing data releases (less important) as well as Core PCE (important) on 31 October which is expected to drop back to 2.6% YOY while rising 0.3 on the month (so decent scope to see a downside miss?)

Barring any shockers here we will drift into a benign 25 bp's cut on 07 November.

But herein lies the problem.

I do not think the economic backdrop looks dramatically different from that seen AT THIS POINT in 2007 or for that matter 2000.

The important point here is that the economy did not just roll over the edge of a cliff, it was pushed.

In 2000 that came effectively in 2 stages

1. The collapse of the Dot Com bubble which the Fed was initially slow to react to but when they did, we saw 5 consecutive 50 bp's cuts from Jan to May 2001.

2. 9/11 which changed everything then and since.

In 2007 there were a number of things

The main catalyst was housing and CMBS and the feedback loop into the banking system and real economy as the Fed prevaricated about cutting rates - giving us the GFC.

Today

There is a possibility that AI and the "Mag 7 trades" could be described as somewhat similar to 2000. In reality this rally is not as loved or participated in as then and the markets back then (NASDAQ) in particular just traded like "meme stocks" with a lot of companies having no income let alone no profit.

Looking at 2007 we do not have the backdrop in housing that we saw then. We do not have the massive draw on Equity out of housing. We do not have the leverage on CMBS that were effectively a basket of crap sold as diamonds. We do not at this point have the broad-based banking stresses as then which started to fray as we headed through Q4, 2007.

In both periods the coming months into year-end were when the "wheels began to fall off"

So now, either that is simply not going to happen OR the catalysts are different.

What catalysts do we have?

Politics and the Presidential election where we have likely never been more divisive as we are today. the only common ground seems to be that neither party seems remotely prepared to focus on the "ticking time bomb" of the level of debt we have bult up in the last 2 decades and particularly since 2020.

Geopolitics are at a more fragile point than seen in many years. Russia-Ukraine, Israel-Iran, China-Taiwan to mention the more obvious ones with very real dangers that "unintended mistakes" are made.

The Global economy is stressed Yes, the US economy is holding up and looks like the best house on a bad street but on the back of our debt rising at a faster base than the growth of the economy like a bad hedge fund. Europe is showing no such growth and neither is Japan.

China The economy here looks in dire straits with a big danger that the policy measures are now too little too late. This has both Global economy influences as the world's 2nd largest economy but also potential Geopolitical risks IF a deteriorating economic position increases the "nationalistic fervor" and puts "Taiwan in play"

Oil Could surge on a "non-demand" driven basis if the situation with Israel and Iran escalates causing a sharp "fiscal like drag" on the US and Global economies.

CRE and Regional banks are in the background at the moment but what if rates (longer-term) do not turn lower like in 2007 but start to head higher again. That would also have implications for Treasury funding and the P&L of the fed's balance sheet

A N Other As we know from history sometimes the cause of this "flip" is not obvious until it happens (The crash of 1929, the Asian/Russia/LTCM failures of the late 1990's, The DotCom bubble of 2000, the GFC of 2007, and of course the Russian invasion of Ukraine and the Hamas attack on Israel)

The important thing, however, is at this point all of the above are "tail risks" rather than "core risks" and pre-empting their escalation can be a costly business. Rather you need to wait until the "event risk" moves to be an actual risk in that regard- if it actually does at all.

Of course, if none of this happens it greatly increases the risk that all aspects of the 1990, 2000 and 2007 analogs will break down.

That has not happened YET, but Q4, 2024 is clearly setting up as the pivotal point in this cycle where we will see whether "History Rhymes " yet again or whether "It's different this time.

Hopefully the price action we see in the coming weeks can further guide us in that respect.