After an amazingly volatile time in markets over the last 2 weeks it feels like a good time to stand back, smell the roses, and reflect on the big picture.

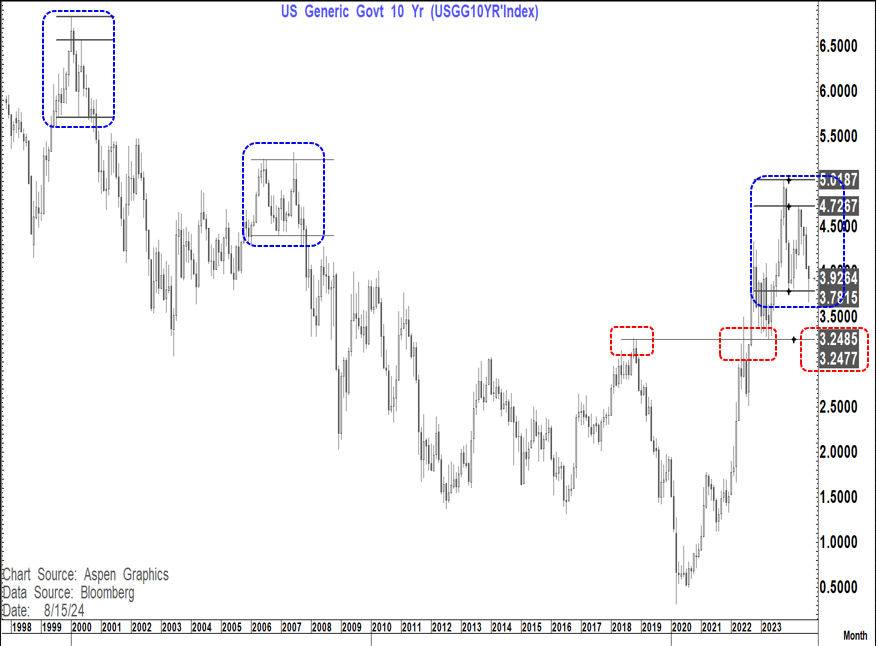

In that respect the 10-year yield chart below is worth looking at.

As readers will know 2000 and 2007 remain my roadmaps until proven otherwise (With the 6 Sept employment data a key linchpin in that respect)

Ahead of that is is worth once again looking at those periods to see that path and timing of moves into year end.

Firstly my bias remains that we can see a move down to 3.25% on the US 10-year yield. Even if that view is correct the path and timing remains equally important.

For that I still see those 2000 and 2007 roadmaps as the best guides right now. So let us look at those pictures.

In 2000 we saw the 10-year yield peak, fall sharply, and rally back up to the 76.4% pullback level in May of that year. Yields then fell sharply and moved below that first low in August 2000 but did not sustain below on a monthly close basis.

In fact we saw yields chop around for a number of months with the first monthly close below taking place in November that year in a sharp fall that took us into March 2001.

After trading below that support in August the highest we saw yields trade above that support area between August and November 2000 was 21 bp's.

In 2007 we had a similar if slightly different picture. We saw the 10-year yield peak, fall sharply, and rally back up to create a double-top in June of that year. Yields then fell sharply in July and August and moved below that first low in Sept 2007 but did not sustain below on a monthly close basis.

In fact we saw yields chop around for a number of months with the first monthly close below taking place in November that year in a sharp fall that took us into Jan 2008

After trading below that support in Sept the highest we saw yields trade above that support area between August and November 2000 was 32 bp's.

In 2024 we have had a combination of those 2 pictures. We saw the 10-year yield peak, fall sharply, and rally back up to create a 76.4% pullback in April this year. Yields then fell sharply into August and moved below that first low in but did not sustain below on a monthly close basis (so far)

After trading below that support the highest we have seen yields trade above that support area so far has been 25 bp's to 4.02% with some good resistance now at 4.02-4.03%.

That is a slightly bigger bounce than seen in 2000 (21 bp's above the pivot) and less than 2007 (32 bp's above the 3.78% pivot - that would equate to 4.10% with very good resistance at 4.14%.

A sustained downside move below 3.78-3.81% would be the signal for the move towards 3.25% (2018 trend high) and acceleration point on the way up in 2022- Likely by Dec-Jan.

Of course the big "Elephant in the room" in this scenario is likely the Employment picture and historically in particular the numbers posted in August 2000 and 2007 (Sept release). A weak number then became a clear catalyst for the eventual move lower in yields that gathered pace in November.

IF we see a weak employment report on 06 sept this year then the paths above are very much in play. IF not then we need to question whether it may indeed be different this time.

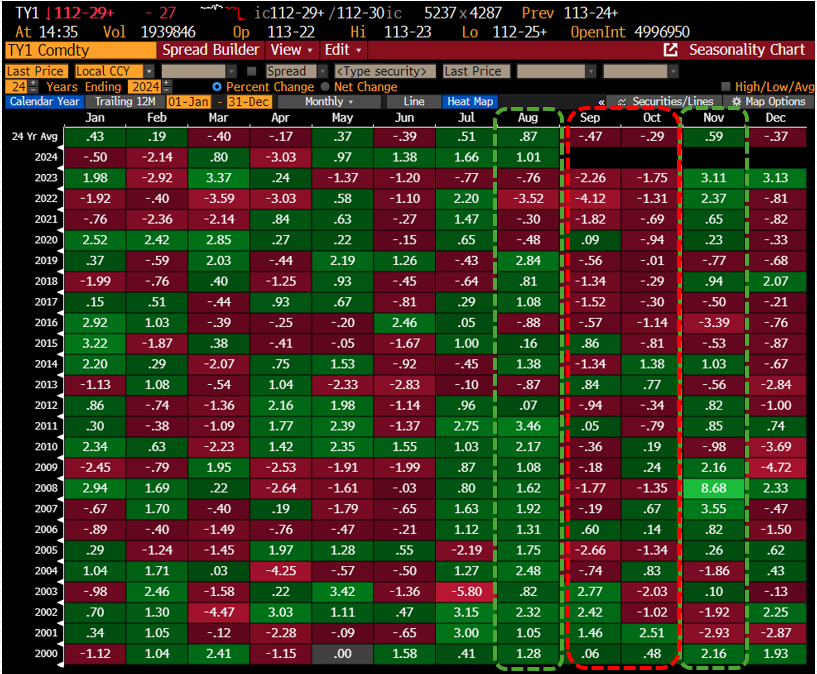

It is also worth looking at the seasonality of TY1 since 2000- in August, Sept, Oct ,Nov

August is seasonally the strongest month of the year. Including this year (so far) it is up on average .87% and 76% of the time.

September is historically the worst month of the year falling .47% and 62% of the time.

October is historically negative also falling .29% and 63% of the time

November is historically the 2nd best month of the year after August rising .59% and 63% of the time.

All this suggests we could be in a choppier day to day directionless market for weeks if not months before we see the next trending move develop.

At this point the bias is that when it happens that move will be for lower yields with November being the prime month for that rally to begin in earnest.

Until then we may be about to see a lot of noise.